How to Choose the Right MCA Funding Source for Your Brokerage

The funding source you choose shapes everything about how your brokerage runs, from approval speed to commission reliability to how much control you actually have over your own deals. Most brokers figure this out the hard way, after months of slow approvals, unexplained declines, and commission checks that don’t add up. The MCA funding source you pick is not just a vendor decision, it’s the operational backbone of your entire business.

Brokers who’ve spent time in broker chains or relying on marketplace platforms often describe the same experience: you submit a deal, then wait. You follow up and get vague updates. The merchant loses patience. And when the deal finally closes, the commission is smaller than expected with no real explanation. That’s not a coincidence. It’s the predictable result of how those funding structures are built.

This guide breaks down the four main funding source types available to ISO brokers, what each one actually costs you in time and income, and what to look for before you commit to any funding relationship. By the end, you’ll have a clear framework for building a funding stack that gives you speed, visibility, and commission structures that hold up at scale.

The four types of MCA funding sources brokers actually use

Most brokers know multiple funding options exist, but few have a clean mental model of how they differ structurally. That clarity matters, because the structure determines the speed, the payout, and how much control you actually have over your own deals.

Direct funders hold the capital and make underwriting decisions internally. There are no additional parties between your submission and the funding approval. This is the shortest path from deal submission to funded merchant, and the one that gives brokers the most visibility into why a deal was approved or declined.

MCA marketplace platforms aggregate multiple funders and use automated matching to route submissions. They offer breadth but insert a processing layer between the broker and the actual decision-maker.

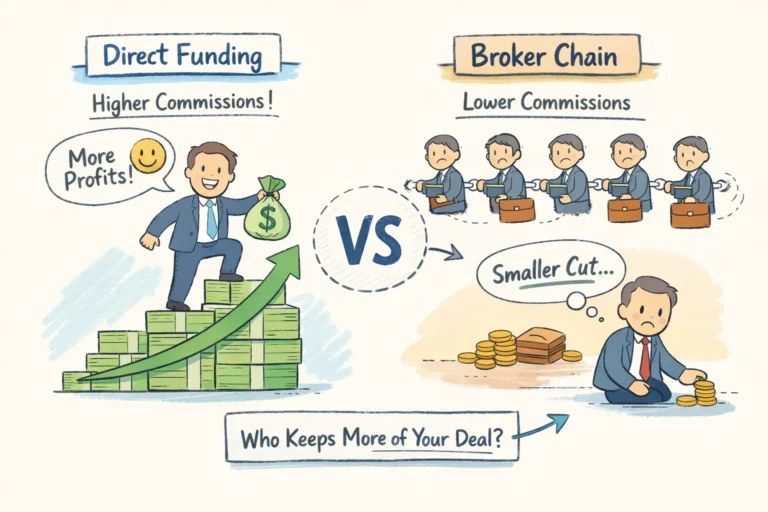

Broker chains occur when one broker submits a deal to another broker, who then passes it upstream. Each layer takes a cut and adds time, and the originating broker often has no idea where the deal actually lands.

Syndication networks pool capital from multiple investors to fund a single deal, which creates a more complex approval process, multiple stakeholders may need to align before a decision is made. Each of these structures carries different implications for your commissions, turnaround times, and access to alternative business funding across deal types.

Direct funders: what a real MCA funding source relationship changes for your brokerage

Speed is the most immediate difference. When a single entity owns the underwriting process, decisions happen faster. Direct funders with streamlined internal operations can turn around credit decisions in a fraction of the time it takes a multi-layered chain. For brokers, faster decisions mean less time babysitting a deal in limbo and more time sourcing the next one.

Commission clarity

Commission clarity is the second major advantage. Direct funders pay commissions directly to the broker with no intermediary taking a percentage along the way. Based on current market norms, direct funder commissions typically run 8, 12% on first-position deals, with strong merchants or higher-volume brokers reaching 15% or more. The best direct funder relationships disclose payout structures before a single deal is submitted, no guesswork, no post-funding surprises, and no commission negotiations happening above your head.

Underwriting transparency

The third advantage is underwriting transparency, which most brokers don’t realize they’re missing until they experience it. Most funders treat their approval criteria like a trade secret, leaving brokers to guess which deals will stick. Direct funders who actually want broker partners share those criteria upfront, which eliminates the wasted effort of packaging deals that were never going to get funded. That transparency alone can recover hours of lost work every week.

Greenvest operates as a direct funder in this model, providing brokers with approval benchmarks before deals are submitted and a clear commission schedule from day one. That kind of operational visibility is what separates a real funding partner from another layer in someone else’s chain.

MCA marketplaces: what you gain in breadth, you give up in control

Marketplace platforms aren’t fraudulent. They’re a different trade-off, and it’s worth understanding exactly what that trade-off is before you build your pipeline around one.

Platforms like Lendio, which connects merchants to dozens of MCA lenders through automated matching, send broker submissions to multiple funders simultaneously. The upside is access to a wider range of merchant cash advance options without individual relationship-building. The downside is that the broker has less control over which funder sees the deal, what criteria are applied, and how quickly a decision comes back. When you don’t know who’s reviewing your deal, you can’t advocate for your merchant or anticipate what additional documentation might be needed.

Commission structures on marketplace platforms are also worth scrutinizing. Marketplaces earn revenue through lender partnerships, which creates an economic incentive to route deals toward preferred partners rather than the best fit for the broker’s merchant. Brokers working with marketplaces typically earn less per deal than in a direct relationship, even after accounting for the convenience of broad funder access. The platform’s economics and the broker’s economics are not always aligned.

It’s also worth noting how MCA financing differs structurally from products like invoice factoring, in revenue-based financing arrangements like MCAs, repayment is tied to future receivables rather than specific invoices, which means the factor rate and effective MCA APR are determined at the funder level. When a marketplace routes your deal, you lose direct insight into how those terms are being set.

Broker chains and syndication networks: where your commission goes quiet

Broker chains are the most common source of silent income loss in this industry. Every additional broker in the chain extracts a portion of the commission before it reaches the originating ISO. A deal that starts with a 12-point commission can arrive at the actual funder as a 4-point deal after two or three hands have touched it, an illustrative but realistic outcome given how sub-broker splits typically work. The originating broker often has no idea this is happening, because no one in the chain has an incentive to disclose it.

The time cost compounds the income cost. A deal that could be funded in 24 hours through a direct funder can take significantly longer moving through a multi-tier chain, each layer adds a communication delay, a re-packaging step, and another set of eyes reviewing terms. For merchants who need capital quickly, that extended timeline is often the difference between closing the deal and losing the merchant to another broker.

Syndication networks operate differently but create their own friction. They allow brokers to access deals outside a single funder’s risk appetite, useful in theory, but the multi-stakeholder structure means approvals require alignment from multiple investors. For brokers focused on volume and speed, that decision timeline is a practical obstacle, particularly for time-sensitive merchant requests. Add in the commission dilution that comes with multi-party profit splits and the limited transparency at renewal, and syndication networks carry real cost for high-volume brokers.

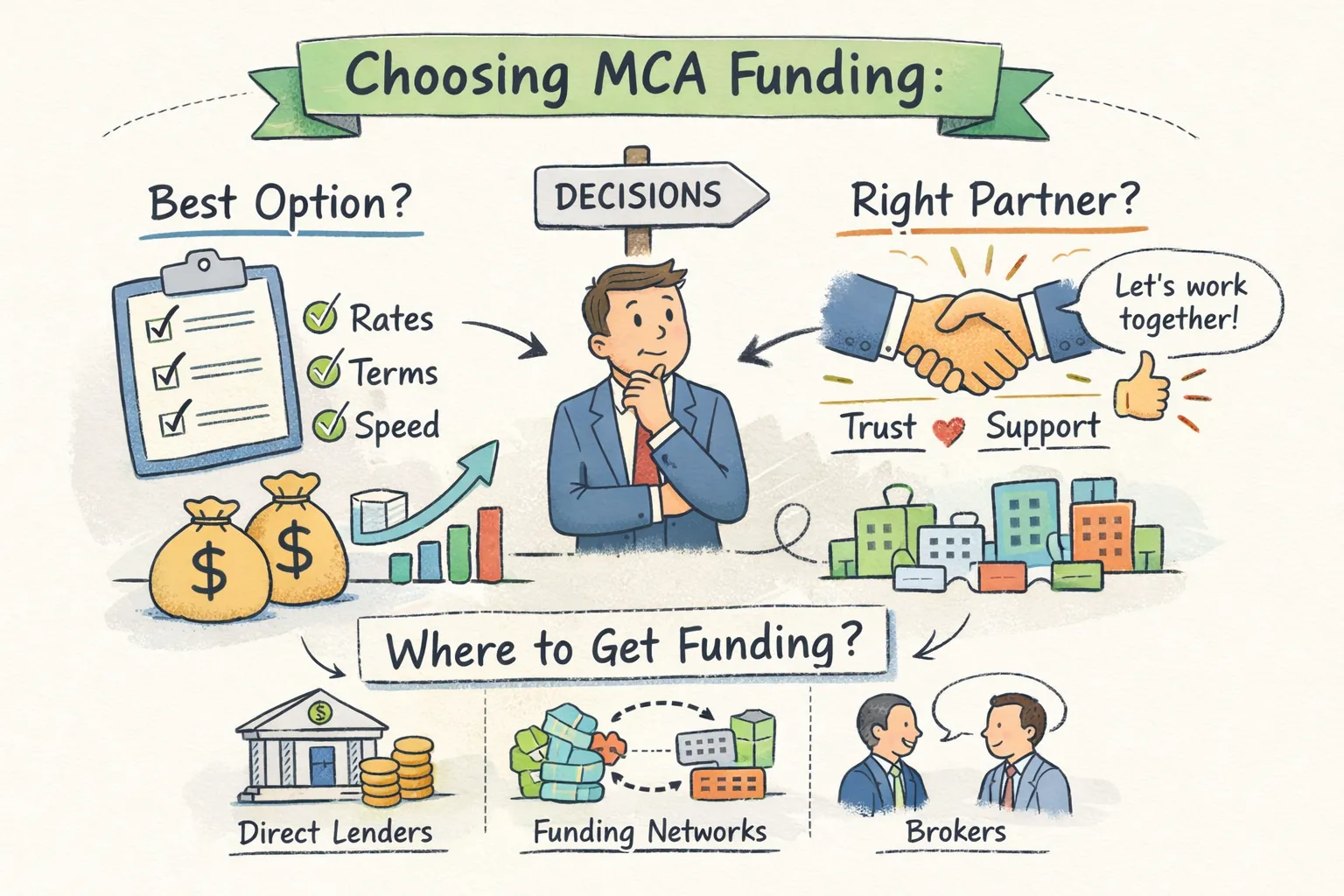

What to look for before you commit to any MCA funding source

Most brokers default to whoever responds to their outreach first. That’s how they end up in broker chains without realizing it. A short evaluation framework prevents that mistake.

Before the first deal, ask any prospective funding partner these five questions:

- How long does it take to receive a credit decision after submission?

- Can you share your commission structure and approval benchmarks upfront?

- Who makes the actual underwriting decision on submitted deals?

- Do you offer both first and second position funding?

- What operational support do you provide beyond capital?

These questions do two things: they surface the information you need to make a real decision, and they expose funders who can’t answer them. A funder that gives vague answers on commission structure or can’t explain their own underwriting criteria is almost certainly not a direct funder. They’re a layer in someone else’s chain.

Specific red flags to watch for: no direct point of contact on the credit team, pressure to submit deals before terms are disclosed, inability to name who deposits funds into the merchant’s account, and no track record of legal filings against defaulted merchants. Legitimate direct funders should be able to address each of these, and if a prospective partner can’t, that’s a strong signal you’re not dealing with a direct funder regardless of what they call themselves. It’s worth requesting documentation, checking state licensing records, and running a small test deal before committing volume. Regulatory frameworks including UCC filings and state disclosure requirements provide additional tools for verifying a funder’s legitimacy.

Building a direct-first MCA funding source stack that scales with your volume

Brokers who consistently hit high monthly deal volumes typically anchor around one primary direct funder relationship and maintain one or two backup options for deals outside their primary partner’s sweet spot. This isn’t about limiting access to capital. It’s about knowing exactly who makes the decision, what they need to say yes, and how fast you’ll hear back. That predictability compounds as your volume grows.

The best direct funder relationships go beyond capital. Greenvest pairs direct funding, working capital from $100K to $5M, with ISO broker support infrastructure: CRM tools and deal tracking to manage your pipeline, plus ongoing training resources for brokers scaling toward higher monthly volumes. Where most funders hand you capital and step back, Greenvest builds in the operational support that typically slows growing brokerages down. A commission modeling tool also gives brokers a concrete way to project earnings before submitting deals, the kind of visibility that changes how you prioritize your pipeline and talk to merchants.

Your funding source is a structural decision, not a sourcing task

Broker chains and marketplaces have their place, but they carry trade-offs in commission, speed, and visibility that compound as your volume grows. Direct funders eliminate the layers that cost brokers the most: time, income, and deal-level control. That math gets more significant every month you’re running at volume.

Start with one diagnostic question: do you actually know who is making the underwriting decision on your deals right now? If the answer is unclear, that’s the problem worth solving first. Not your marketing, not your outreach scripts. The funding relationship itself.

The right MCA funding source won’t just fund your deals faster. It gives you the visibility and commission structure to build a brokerage that doesn’t depend on hoping the next layer up does the right thing. If that’s the kind of partner relationship you’re looking to build, Greenvest’s ISO partner program is a strong place to start that conversation.